Pending Home Sales Break a Five-Year March Losing Streak

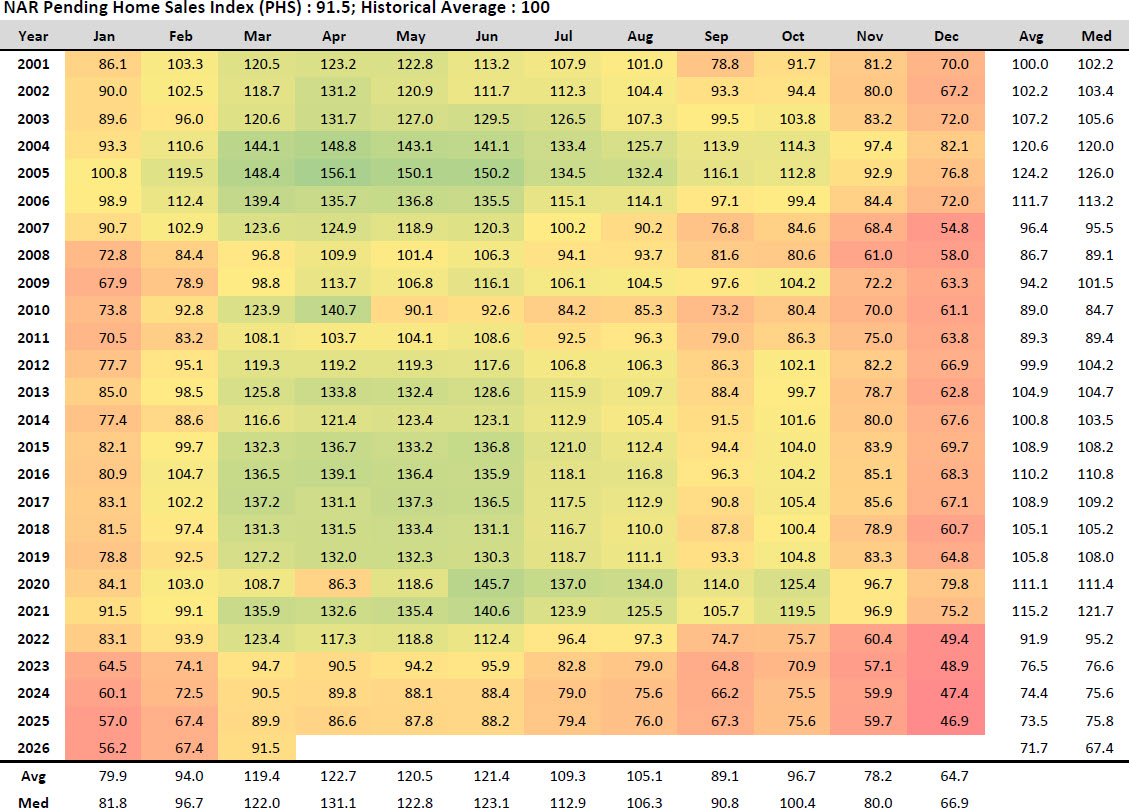

For the first time since the boom of early 2021, the U.S. housing market posted a positive March in pending home sales. The National Association of Realtors' Pending Home Sales Index (PHS) registered 91.5 in March 2026, up 1.8% compared to March 2025. It's a small number on the surface, but it carries weight. March has been one of the most punishing months for the housing market over the past five years, and this is the first time since 2021 that the month closed in the green on a year-over-year basis.

The Pending Home Sales Index tracks signed contracts on existing homes, making it one of the most forward-looking indicators in residential real estate. Because a pending sale typically closes within 30 to 60 days, the PHS offers a preview of closed sales activity heading into the spring and early summer. At 91.5, the index remains below its historical baseline of 100, but the direction has shifted. That shift matters for anyone watching the national housing market, and it also sets the tone for regional markets across the country.

Five Straight Years of March Declines, Now Broken

To understand why a 1.8% year-over-year increase is noteworthy, you have to look at what came before it. March 2022 posted a 9.2% annual decline. March 2023 collapsed 23.3% year over year, one of the steepest March drops in the index's history. March 2024 fell another 4.4%, and March 2025 slipped again by 0.7%. Four consecutive years of deterioration, followed by a marginal but meaningful reversal in March 2026.

The last positive March reading came in 2021, when the index surged 25.0% year over year to 135.9 during the pandemic-era buying frenzy. That reading was an outlier driven by extraordinary conditions, including historically low mortgage rates, shifting household preferences, and limited supply. The 2026 reading is a very different story. It doesn't reflect a buying frenzy. Instead, it suggests the market has finally found a floor after a multi-year correction and is beginning to stabilize at a lower baseline.

Context: Where 91.5 Sits in the Bigger Picture

While March 2026 broke the negative streak, it's important to keep the number in perspective. The index reading of 91.5 is still 8.5% below the historical benchmark of 100, which NAR set based on a level of contract activity consistent with a healthy housing market. Compared to the long-term March average of 119.4, March 2026 is 23.3% below normal. And compared to the all-time March peak of 148.4 set in 2005, the current reading is 38.3% lower.

In other words, the market is no longer sliding, but it hasn't recovered either. It's holding a position well below its historical mean, and that plateau has now persisted for three consecutive years. March 2024 came in at 90.5, March 2025 at 89.9, and March 2026 at 91.5. The gap between these three readings is narrow, which reinforces the idea that the market has entered a phase of stability rather than expansion.

What's Driving the Shift

Several forces help explain why pending sales have stopped falling and begun to tick higher. Mortgage rates have come off their 2023 highs, which has eased some of the affordability pressure that pushed buyers to the sidelines. Inventory levels have improved in many markets compared to the depths of the 2021 and 2022 shortages, giving buyers more options and reducing the intensity of bidding competition. Consumer confidence in the housing market has also firmed as the gap between sellers' expectations and buyers' realities has narrowed.

At the same time, pent-up demand from buyers who delayed purchases during the high-rate environment is finding its way back into the market. First-time buyers, move-up buyers, and relocators who paused their plans over the past two years are now re-entering at a measured pace. The 1.8% year-over-year gain in March 2026 reflects that gradual return rather than a sudden rush.

The Monthly Pattern Is Normal for Once

March is historically the strongest pending sales month of the year, reflecting the standard onset of spring buying. The 35.76% month-over-month jump from February 2026 to March 2026 falls in line with the historical March pattern. The long-term average March month-over-month change is 27.3%, and the median is 28.9%. That means this year's March bounce was slightly stronger than the typical seasonal lift, not weaker. When you combine that with the year-over-year gain, the signal becomes clearer. The market is behaving more like its historical self this year than it has in a while.

The January through March cumulative index for 2026 stands at 215.1, which is 0.4% higher than the same stretch in 2025. That's the first positive first-quarter read since 2021 as well. First-quarter activity is often the most reliable early read on annual direction because it captures buyer decision-making heading into the peak selling season. A flat-to-positive Q1 does not guarantee a strong year, but it removes one of the major downside signals that has defined the market since 2022.

What to Watch Next

The months ahead will determine whether March's positive print becomes the start of a real recovery or a single data point in an otherwise flat trend. Historically, the index declines month over month in April from March levels, with an average April drop of 1.0% and a median of essentially zero. That makes the April 2026 reading particularly important because it will test whether the momentum from March carries forward or whether the spring surge was a one-off.

May and June readings will also matter because they capture the core of the spring and early summer buying season. If the year-over-year trend stays positive through those months, it will confirm that the housing market has moved into a genuine recovery phase rather than simply stabilizing at a lower level. If those months turn negative again, the March print will look more like noise than signal.

For now, the takeaway is straightforward. Pending home sales broke a five-year March losing streak. The index remains well below historical norms, but the direction has changed. After years of watching this indicator fall, the market finally has a positive March to point to, and that matters for how buyers, sellers, and industry professionals are reading the current environment.

Frequently Asked Questions

What is the NAR Pending Home Sales Index?

The Pending Home Sales Index, published by the National Association of Realtors, measures signed contracts on existing homes that have not yet closed. It's considered a leading indicator for the housing market because pending sales typically convert to closed transactions within 30 to 60 days. The index uses a baseline value of 100, which represents the level of contract activity in 2001. Readings above 100 indicate stronger-than-baseline activity, while readings below 100 indicate weaker activity. The index is widely tracked by economists, investors, and real estate professionals as an early signal of where the housing market is headed.

Why does a 1.8% year-over-year gain matter?

The 1.8% increase matters because it represents the first positive March reading since 2021. From 2022 through 2025, March pending home sales fell every single year compared to the prior year, including a 23.3% collapse in 2023. A positive March reading in 2026 signals that the market's downward trajectory has ended, at least for now. While the gain itself is modest, the directional change is what carries weight. Small positive movements after a prolonged decline often mark inflection points in housing cycles, making this reading a potentially important data point for forecasting the rest of 2026.

Is the housing market recovering or just stabilizing?

The data suggests the market is stabilizing rather than entering a full recovery. The March 2026 reading of 91.5 is only marginally higher than March 2024 at 90.5 and March 2025 at 89.9, which indicates a tight band of activity over three years. A true recovery would typically involve the index returning closer to its historical baseline of 100 or higher, and March 2026 remains 23.3% below the long-term March average of 119.4. Stabilization is still meaningful because it signals the end of the downturn, but buyers and sellers should understand that activity levels remain well below historical norms.

What do pending home sales tell us about closed sales in coming months?

Pending home sales are one of the most reliable leading indicators for existing home sales because a contract typically closes within 30 to 60 days of being signed. That means the March 2026 Pending Home Sales Index reading provides a preview of closed existing home sales in April and May 2026. If the pending sales trend holds, closed sales should show similar year-over-year stabilization in the next couple of monthly reports. However, pending contracts can fall through due to financing issues, inspection problems, or appraisal gaps, so the conversion rate from pending to closed is not always one-to-one.

How does the current index compare to the all-time March peak?

The all-time March peak for the Pending Home Sales Index was 148.4, set in March 2005 at the height of the pre-recession housing boom. March 2026's reading of 91.5 is 38.3% below that peak. That gap reflects both the extraordinary conditions of the mid-2000s and the more constrained environment of recent years, characterized by higher mortgage rates, affordability challenges, and tighter inventory in many markets. While the peak isn't a realistic near-term benchmark, it helps illustrate just how far current activity sits from the most active period in the index's history.