How Austin Compares to Other Major Real Estate Markets: October 2025 Analysis

Published | Posted by Dan Price

The latest October 2025 housing data shows Austin falling behind other major real estate markets as rising supply and declining sales shift the market further toward buyer control. While many metro areas are managing to sustain near-flat demand or moderate absorption, Austin is seeing a more pronounced pullback, indicating that the correction phase is further advanced locally. With sales down nearly ten percent and inventory levels climbing rapidly, the market now requires highly strategic pricing and positioning for sellers to remain competitive. In today’s environment, understanding how Austin compares to similar fast-growth markets is essential for interpreting where local housing trends are headed next.

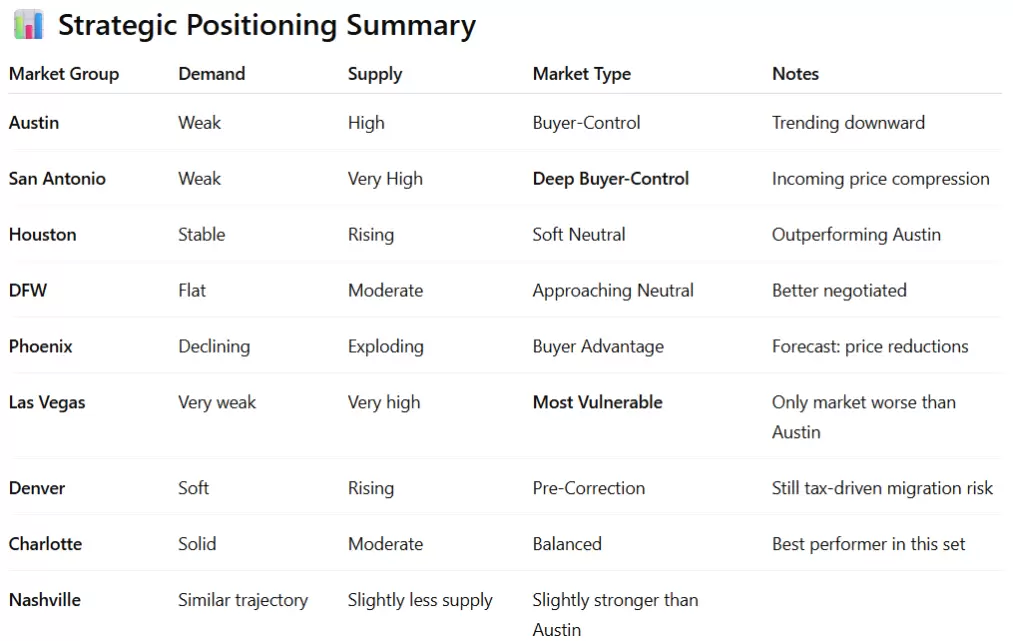

Austin recorded 2,238 closed sales in October 2025, a 9.6 percent decline from last year and nearly a 20 percent reduction from October 2019. Nationwide, closed sales increased 1.5 percent over the same period, and markets such as Charlotte and Nashville remained relatively stable. San Antonio experienced a similar sharp decline at 9.8 percent, while Phoenix and Denver posted modest declines closer to two to three percent. Only Las Vegas performed worse than Austin in long-term comparison, with closed sales down nearly 38 percent versus 2019 levels. This places Austin among the weakest-performing markets in terms of demand, signaling that buyers are exercising caution and higher selectivity due to affordability and payment pressure.

Inventory growth further separates Austin from stronger regional competitors. Active listings rose 14.5 percent year over year and now sit 32.9 percent above 2019 levels, indicating slower turnover and longer time on market. Months of supply reached 5.9, marking a clear transition into buyer-controlled territory based on Team Price classifications. In comparison, Nashville, Charlotte, and Denver range from three to four months of inventory, reflecting more favorable balance between supply and demand. Even Dallas–Fort Worth, at 4.7 months, maintains stronger absorption than Austin. The only major market with a higher supply imbalance is San Antonio at 6.4 months, highlighting a broader Texas trend of buyer leverage, but Austin’s simultaneous drop in sales differentiates it as more vulnerable.

New listings increased 8.2 percent year over year in Austin, reflecting seller confidence in the long-term appeal of the market. However, this increase is not translating into buyer urgency, and the widening gap between active inventory and closed sales reflects inefficiency in conversion. While this gap is common during shifting market cycles, Austin’s position relative to peers suggests a more pronounced pricing reaction may be necessary heading into 2026. San Antonio saw listing surges of more than 50 percent, which could increase downward pricing pressure regionally as buyers compare across Texas markets. Houston and Dallas showed more controlled new listing trends, and combined with better sales absorption, these markets appear better positioned to avoid deeper correction.

Historical context further reinforces the trajectory of the Austin real estate market. During the peak acceleration phase between 2020 and 2022, inventory dropped significantly as buyer demand surged. The current reversal indicates that Austin’s return to statistical balance may not be complete until pricing realigns with affordability metrics, especially in relation to income levels and payment-to-principal cost ratios. Unlike Phoenix, which shows similar supply expansion but retains stronger absorption, Austin is advancing through correction sooner. Without an improvement in absorption rates or a trigger event to reset buyer confidence, gradual value compression is likely as the market moves toward equilibrium.

Buyers entering the Austin housing market today have increased leverage and more time to make decisions. For sellers, success now depends on launching correctly priced listings that align with current absorption trends and recent market shifts. Properties that attempt to maintain peak-era pricing are at a higher risk of multiple price adjustments, extended days on market, and reduced negotiating power. Homes positioned ahead of the trendline continue to move, supported by buyers seeking value rather than urgency. Agents must guide clients using precise data interpretation rather than relying on trailing comparables, especially in areas with expanding competition.

Looking forward, Austin’s market conditions point toward further transition, especially if inventory continues to outpace buyer demand into the first quarter of 2026. While long-term demand drivers remain intact, including population inflow and strong employment sectors, the current data-driven environment requires a sharper approach to value positioning. Austin still holds strong potential compared to deeply volatile markets like Las Vegas, but must move decisively to avoid extended stagnation.

FAQ Section

1. How does Austin compare to other major housing markets right now?

Austin is currently underperforming most comparable cities, with closed sales down 9.6 percent year over year and supply at 5.9 months. Cities like Charlotte and Nashville are holding closer to balance, while San Antonio and Las Vegas show similar pressure but in different phases. Austin is further along in correction and requires more aggressive pricing strategy.

2. Is the Austin real estate market currently favoring buyers or sellers?

The market favors buyers due to elevated inventory and declining absorption. With 5.9 months of supply, Austin is solidly in buyer-controlled territory. High competition and selective buyer behavior are shaping negotiation dynamics.

3. What are the biggest risks for sellers in the current Austin housing market?

The greatest risk is launching at an inflated list price based on trailing comparables. Homes that do not align with current inventory levels and absorption rates are likely to stagnate. Sellers must prioritize market readiness and accurate pricing to prevent extended days on market.

4. Why is Austin’s demand declining even as more listings enter the market?

Higher mortgage payments, affordability concerns, and increased competition are causing buyers to hesitate. New listings increased 8.2 percent year over year, but sales did not follow, causing supply buildup and weakening urgency among buyers.

5. How should agents prepare for early 2026 market conditions in Austin?

Agents should anticipate increased negotiation pressure and potential for continued price correction. Focus should shift toward value-based positioning, strong pricing discipline, and proactive buyer engagement strategies. Listings that launch with accurate pricing and condition alignment will be best positioned to capture demand.