Austin Suburbs Lead Nation in Rent Declines as Texas and Sun Belt Markets Cool

Published | Posted by Dan Price

The Austin housing market is undergoing a clear shift, and the most visible signal is coming from the rental side of the Austin real estate landscape. Cities surrounding Austin are posting some of the sharpest rent declines in the country, and the pattern is not isolated. As rents fall in Round Rock, Georgetown, Leander, Pflugerville, Cedar Park, Kyle, and San Marcos, the broader Texas market is showing the same directionality, followed by similar movements across the Sun Belt and national market. The cooling is not sudden, but the depth and concentration of these declines illustrate how the Austin real estate market is recalibrating after years of aggressive construction, rapid population inflows, and historic pandemic-era pricing.

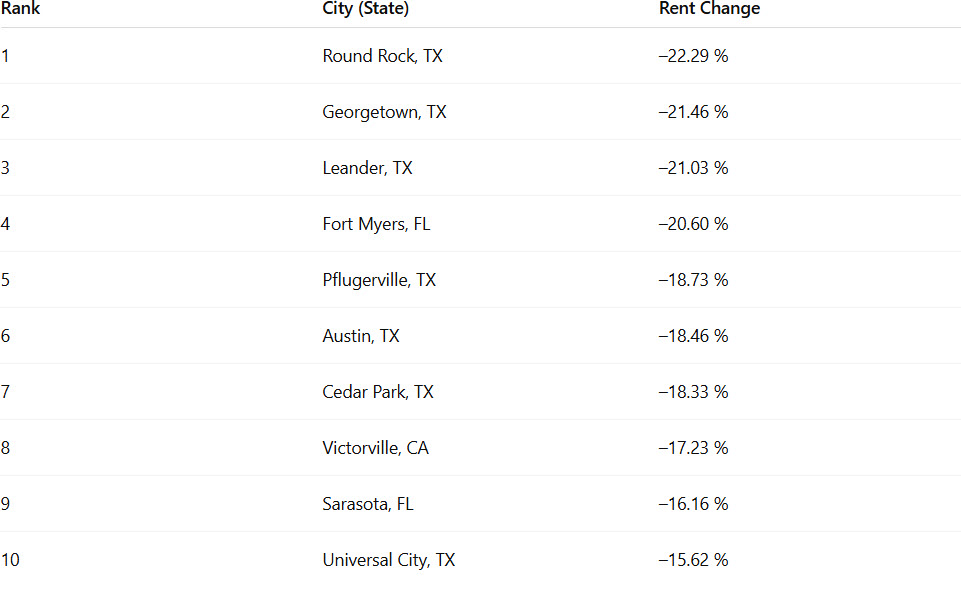

The most striking part of the data is how heavily centered it is around Austin. Round Rock leads the entire nationwide dataset with a –22.29 percent rent decline. Georgetown follows at –21.46 percent, and Leander posts a –21.03 percent drop, placing three Austin suburbs among the top three rent declines in the United States. Pflugerville and Cedar Park register similarly steep movements at –18.73 percent and –18.33 percent. Austin itself is down –18.46 percent, which places the urban core among the ten worst rent drops nationally. These numbers send a clear message: the Austin housing market and its surrounding suburbs are unwinding at a faster rate than most major metros in the country.

This clustering of rapid declines is not random. Austin has been one of the fastest-growing metros for a decade, and developers responded with substantial multifamily construction. Many of these projects delivered in 2023, 2024, and 2025, creating a supply bulge that continues to absorb into the market. The result is straightforward: when new supply outpaces renter demand, prices correct. The steepness of the correction in the Austin real estate market is a direct reflection of that imbalance. Investors, landlords, and builders are feeling the same pressure, and private owners now find themselves competing directly with thousands of units offering concessions, discounts, and free-rent promotions.

The pattern extends beyond the core suburbs into the broader commuter belt. New Braunfels is down –15.24 percent. Temple shows a –13.04 percent decline. Killeen, part of the extended Central Texas corridor, is down –6.57 percent. Even smaller corridor cities like San Marcos at –14.16 percent and Kyle at –14.73 percent are experiencing meaningful downward pressure. The Austin housing market is therefore not only cooling in the immediate suburban ring; the cooling effect radiates outward well into cities traditionally considered secondary or tertiary to Austin proper.

These declines also signal something about buyer and renter behavior in the region. The rapid price increases of 2020–2022 pulled rents far above long-term trend lines, particularly in fast-growth suburbs. As affordability tightened and economic momentum slowed, renters became more price-sensitive. The Austin real estate market is now seeing a rebalancing phase where the price elasticity of demand is reasserting itself. This is especially true in cities like Round Rock, Georgetown, and Leander, where rent growth had outpaced wage growth for several years. The current declines are not necessarily indicative of distress; they are the logical outcome of reverting to a more realistic equilibrium.

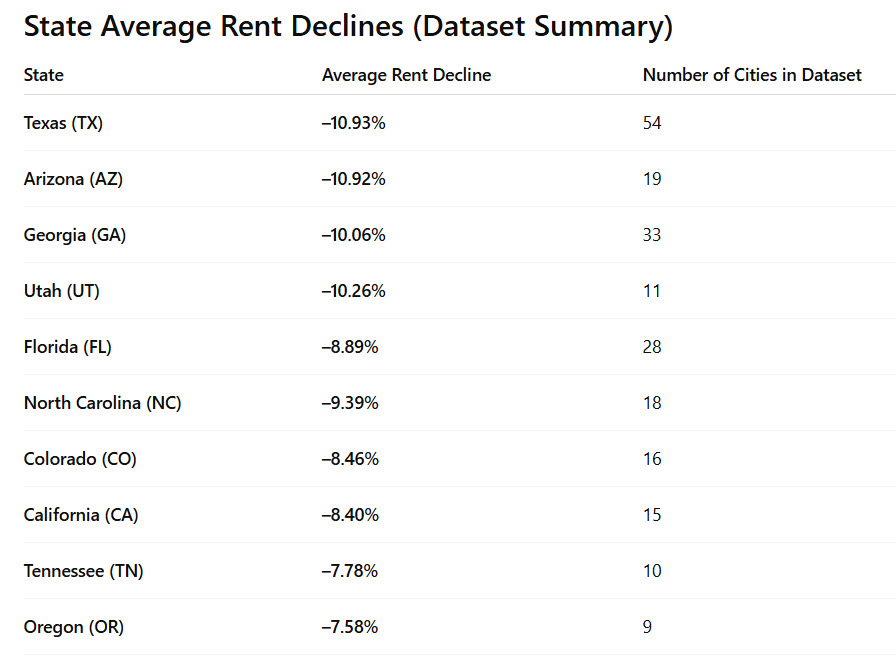

When shifting from Austin-area markets to statewide trends, the picture remains consistent. Texas accounts for 54 cities on the national list of rent declines, more than any other state by a wide margin. The average decline across all Texas markets in the dataset is –10.93 percent. This statewide average reflects not just the Austin region, but also the Dallas–Fort Worth, San Antonio, and Houston metros, each of which shows a large cluster of mid-single-digit to low-double-digit declines. Texas is among the fastest-correcting rental markets in the country because it has been one of the most active construction markets for several years. As new units enter the market and compete for the same renters, prices adjust downward to clear the inventory.

The scale of new construction in Texas also has a multiplier effect. High delivery volume suppresses rent growth; lower rent growth reduces effective yields; lower yields pressure investor demand; and weaker investor demand re-prices the land and development pipeline. Each step reinforces the next. The Austin housing market is currently in the middle of that cycle. Robust supply is helping renters, but it places downward pressure on existing units, particularly those built between 2015 and 2022 that now face direct competition from brand-new buildings.

When zooming out to the national level, the same pattern appears in other high-growth Sun Belt states. Florida shows an average decline of –8.89 percent across the cities in the dataset, with notable drops in Fort Myers at –20.60 percent, Sarasota at –16.16 percent, and Bradenton at –11.72 percent. Arizona is averaging –10.92 percent, supported by declines in Goodyear at –14.55 percent, Glendale at –12.79 percent, Tempe at –9.45 percent, Mesa at –11.27 percent, Scottsdale at –8.40 percent, and Phoenix at –11.83 percent. Georgia, driven by the Atlanta metro, averages a –10.06 percent decline with broad, consistent reductions across suburban markets.

Utah, another high-growth state, registers an average decline of –10.26 percent with notable movements in West Valley City at –15.06 percent, South Salt Lake at –11.28 percent, Taylorsville at –7.05 percent, Murray at –9.65 percent, and West Jordan at –10.30 percent. North Carolina shows similar cooling trends, with Raleigh down –10.61 percent, Charlotte down –7.75 percent, Cary down –7.97 percent, and Wilmington down –7.94 percent. In every case, the markets with the steepest rent declines share the same traits: rapid population growth, aggressive development pipelines, and significant multifamily supply delivery between 2022 and 2025.

Nationally, the pattern is unmistakable. The regions that experienced the fastest rent inflation during the pandemic period — primarily Texas, Florida, Georgia, Arizona, Utah, Tennessee, and the Carolinas — are now posting the steepest corrections. This reflects a natural reversion after extraordinary growth. Rent declines alone do not imply weakness in the long-term outlook; rather, they indicate the reestablishment of balance between supply and demand. The Austin real estate market is a prime example of this recalibration. After years of rapid expansion, the market is normalizing, and the rent declines offer a clearer signal of where pricing power has shifted.

The national trend also illustrates a broader point about the relationship between migration, construction cycles, and affordability. Markets that saw significant in-migration and investor activity during 2020–2022 have now reached a saturation point. Renter demand is no longer accelerating at the same pace, while the number of units under construction remains high. This imbalance creates downward pressure on rents, and that pressure will likely continue until the pipeline thins or population growth re-accelerates. For now, the Austin housing market sits at the center of this adjustment.

FAQ SECTION

What is causing rent prices to fall so sharply around Austin?

The declines are driven primarily by a surge in new apartment supply that entered the market between 2023 and 2025. Developers built aggressively during the pandemic boom, and many of those units are now leasing up at the same time. When new supply outpaces renter demand, the Austin real estate market adjusts through lower rents and increased concessions. This is a normal rebalancing after a period of unusually fast rent inflation.

Are falling rents a sign of weakness in the Austin real estate market?

No. Falling rents indicate normalization, not distress. The pandemic years brought unusually rapid rent growth, and current declines reflect a return to more sustainable levels. Austin’s long-term fundamentals remain strong, but the short-term market is recalibrating as high supply competes for renters and resets pricing power.

How do Austin’s rent declines compare to the rest of Texas?

Austin and its surrounding suburbs are experiencing the steepest declines in the state. While Texas overall averages –10.93 percent rent declines across all cities in the dataset, many Austin-area markets exceed –15 percent. Round Rock, Georgetown, Leander, Pflugerville, and Cedar Park are among the hardest-hit statewide, highlighting the concentration of supply in the Austin metro.

Which states are showing similar rent trends to Texas?

Arizona, Georgia, Utah, Florida, and North Carolina are posting similar double-digit declines in major metros. These states share similar characteristics: rapid in-migration during the pandemic, aggressive development pipelines, and large numbers of new multifamily units hitting the market between 2022 and 2025. Their rent declines mirror the supply-driven cooling happening in the Austin real estate market.

How long will the rent correction continue?

Rent corrections typically last until the supply pipeline slows or demand grows enough to absorb excess inventory. In Austin, many projects are already underway, which means supply will continue to deliver into the market through late 2025 and early 2026. As these units are absorbed, the Austin housing market should stabilize, especially if population growth resumes its pre-2022 trajectory.