Austin Area Pre-Foreclosures, Auctions, and Bank-Owned Properties Growing at 17.2 Per Week

Published by Team Price Real Estate | Austin Area Distressed Property Tracking | March 10, 2026

The Austin real estate market is adding pre-foreclosures, auction properties, and bank-owned homes at a rate of 17.2 per week — and that pace is accelerating. Distressed properties in this analysis are defined specifically as properties in one of three stages of the foreclosure pipeline: pre-foreclosure, scheduled for auction, or already bank-owned (REO). According to distressed property tracking data compiled by Team Price Real Estate, the Austin area recorded 2,198 such properties on September 26, 2025. By January 27, 2026, that number had risen to 2,371. As of March 10, 2026, the count stands at 2,483 — a net increase of 285 properties and a 13.0% jump in just five and a half months.

The Rate Is Accelerating — Not Stabilizing

The total count tells part of the story. The velocity tells the rest. From September 26 to January 27 — a span of approximately 17 weeks — the Austin area added 173 distressed properties at a pace of roughly 10.2 per week. From January 27 to March 10, just 6.5 weeks later, the market added another 112 properties at a rate of 17.2 per week. That is a 69% acceleration in the weekly growth rate between the two tracking windows. The foreclosure pipeline across the Austin housing market is not stabilizing — it is filling faster than it is clearing.

That acceleration is the critical data point for anyone tracking Austin real estate trends in 2026. Pre-foreclosures, auctions, and bank-owned properties represent homeowners and lenders at various stages of financial resolution — and when that pool grows at an increasing weekly rate, it signals that new distress is entering the pipeline faster than existing distress is being resolved through sales, loan modifications, or other outcomes.

Understanding the Three Stages: Pre-Foreclosure, Auction, and Bank-Owned

Every distressed property in this dataset sits at one of three distinct points in the foreclosure process, and each stage carries different implications for buyers, investors, and the broader Austin property market.

Pre-foreclosure is the earliest stage. The homeowner has defaulted on their mortgage — meaning they have missed payments and the lender has issued a formal notice of default — but the foreclosure process has not yet been completed. The owner still holds title to the property and technically has the ability to cure the default, sell the home, or negotiate a resolution with the lender. Pre-foreclosure properties are among the most negotiable in the market because the owner is motivated to avoid the damage of a completed foreclosure on their credit and financial record. For buyers, this stage offers the opportunity to purchase directly from a motivated homeowner, often before the property ever reaches the open market.

Auction properties have moved past the pre-foreclosure window. The lender has completed the legal foreclosure process and the property is scheduled — or has been scheduled — to be sold at a foreclosure auction, typically on the courthouse steps. In Texas, foreclosure auctions are conducted on the first Tuesday of each month. Auction purchases require cash, carry no inspection contingency, and transfer with no seller disclosures — meaning buyers assume whatever title issues or physical condition challenges come with the property. The potential discount can be significant, but so is the risk for buyers who are not experienced with the process.

Bank-owned properties — also called REO, or Real Estate Owned — are homes that did not sell at auction and have reverted to the lender. The bank now owns the property outright and is motivated to sell it to remove the non-performing asset from its books. REO properties are typically listed on the MLS through an asset management company or REO-specialized agent. Banks generally sell as-is with limited disclosures, but the transaction process is more conventional than an auction purchase. REO pricing is set by the bank's internal valuation and asset disposition goals, and in a market with growing inventory like Austin, banks are under increasing pressure to price competitively.

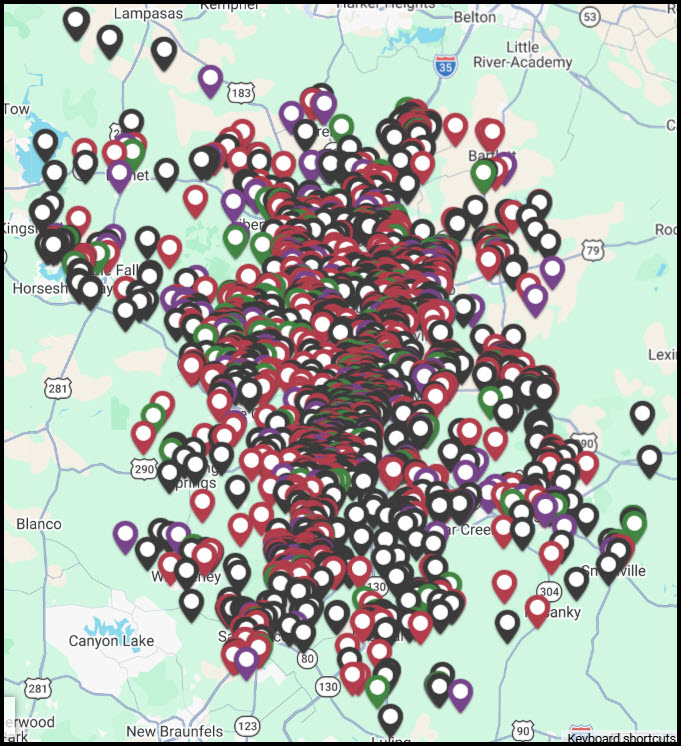

What the Map Reveals: MLS History Across 2,483 Properties

The Team Price Real Estate distressed property map plots all 2,483 properties across the Austin metro and color-codes each one by its MLS history. That layer of data reveals not just where distressed properties are located, but how visible they are — or are not — to the conventional buyer market.

Green pins mark distressed properties that are currently active on the MLS. These are pre-foreclosures, auction properties, or bank-owned homes that have an active listing right now and are visible to every buyer and agent searching the market. Active distressed listings create direct, immediate pricing competition for non-distressed inventory in the same neighborhoods.

Red pins identify properties that had prior MLS activity at some point — a past sale, lease, or listing — but are not currently listed. These are distressed properties with a market history that have not yet re-engaged with the MLS in their current distressed state. The prior MLS connection means the owner has some familiarity with how the market works, even if they have not yet chosen to list.

Purple pins represent properties where a listing was placed on the MLS but expired without resulting in a sale or lease. A distressed property with an expired listing is a particularly telling profile — the owner attempted the conventional market route, was unsuccessful, and is still in financial difficulty. Expired listings in distress often reflect properties that were overpriced for their condition, needed work that deterred buyers, or were listed during an unfavorable market window.

Black pins are the most strategically significant category in the dataset: distressed properties that have never appeared on the MLS at any point in their history. No listing, no sale, no lease — these are homeowners navigating pre-foreclosure, auction, or REO status who have had zero engagement with the traditional real estate market. For investors and buyers pursuing off-market acquisitions in the Austin area, the concentration of black pins across the metro map defines exactly where that completely untapped distressed inventory exists.

Geographic Reach: Metro-Wide, Not Isolated

The distressed property map shows activity spanning the full Austin metro footprint. The highest density cluster sits in and around the urban core, with meaningful distribution radiating outward through every major growth corridor. Georgetown, Round Rock, Pflugerville, Cedar Park, Leander, Kyle, Buda, and San Marcos all carry visible distressed property concentrations. The Hill Country communities to the west show sparser activity, while the eastern corridor through Manor, Elgin, and toward Bastrop reflects a notable distressed presence consistent with those markets' affordability profiles and homeowner demographics.

The breadth of the geographic distribution is itself a data point. This is not a localized stress event concentrated in one sub-market or one price tier. Pre-foreclosures, auctions, and bank-owned properties are accumulating across communities at every price point in the Austin real estate market — from outer-ring affordable suburbs to mid-tier growth corridors to higher-end Hill Country communities. That pattern is consistent with a market where elevated mortgage rates and extended days on market have applied financial pressure broadly, not selectively.

What 2,483 and Growing Means for the Austin Housing Market

A distressed property count of 2,483 — growing at 17.2 per week and accelerating — is a meaningful leading indicator for the Austin housing market heading into spring 2026. Distressed properties at this volume and growth rate represent a building inventory of motivated sellers that exists alongside the 13,813 active listings already tracked in the Austin Area MLS. As more pre-foreclosure properties either get listed or proceed to auction, and as bank-owned inventory grows, the competitive pressure on traditional sellers increases.

For buyers, the trend is directionally favorable — more distressed inventory means more opportunities to negotiate, more motivated sellers, and more properties entering the market at or below market value. For sellers pricing non-distressed homes in neighborhoods where distressed properties are concentrated, the comps generated by foreclosure sales will be a factor in appraisals and buyer negotiations. And for the Austin real estate market overall, the trajectory of this data between now and mid-2026 will be one of the clearest signals of whether underlying financial stress is peaking or continuing to build.

Frequently Asked Questions

What are the three stages of a distressed property in real estate?

The three stages of a distressed property follow the foreclosure pipeline in sequential order. Pre-foreclosure is the first stage, triggered when a homeowner defaults on their mortgage and the lender issues a notice of default — the owner still holds title and can potentially sell or resolve the default before it progresses. Auction is the second stage, where the property has been foreclosed upon and is scheduled to be sold at a public foreclosure auction, in Texas held on the first Tuesday of each month. Bank-owned, or REO (Real Estate Owned), is the final stage — the property did not sell at auction and has reverted to the lender, who now owns it outright and is motivated to sell it to remove it from their books. All 2,483 distressed properties tracked in the Austin area MLS data fall into one of these three categories.

Are foreclosures increasing in Austin in 2026?

Yes. The combined count of pre-foreclosures, auction properties, and bank-owned homes in the Austin area has risen from 2,198 in September 2025 to 2,483 as of March 10, 2026 — a 13.0% increase in approximately five and a half months. The weekly rate of new distressed property additions has accelerated from 10.2 per week in the September-to-January window to 17.2 per week in the most recent tracking period. That 69% acceleration in weekly growth rate indicates the foreclosure pipeline is expanding, not contracting, in the current Austin housing market environment.

How do foreclosures affect Austin home prices?

Foreclosures affect Austin home prices most directly through the comparable sales data they generate when they transact. Bank-owned properties and auction sales that close at below-market prices become data points that appraisers use to establish value for nearby non-distressed homes. In neighborhoods with high concentrations of distressed listings, this can apply measurable downward pressure on surrounding property values. Pre-foreclosure sales — where a motivated owner sells before the bank completes the foreclosure — also tend to price aggressively, producing similar comp impact. The greater the density of distressed transactions in a given area, the more pronounced the effect on Austin real estate market valuations in that submarket.

Can you buy a pre-foreclosure home in Austin before it goes to auction?

Yes, and pre-foreclosure is often the most favorable stage for buyers to engage. During pre-foreclosure, the homeowner still holds title and can negotiate a sale directly with a buyer, allowing for standard purchase contract terms including inspections, financing contingencies, and title insurance. The owner is typically highly motivated to sell because completing a transaction before the foreclosure is finalized protects their credit and may allow them to recover some equity. In Texas, the pre-foreclosure window between a notice of default and the scheduled foreclosure auction can be relatively short, so buyers interested in pre-foreclosure properties in the Austin area need to be prepared to move quickly once they identify an opportunity.

What is an REO property and how is it different from a foreclosure auction?

An REO (Real Estate Owned) property is a home that went through the full foreclosure process, was offered at auction, and did not sell — leaving the lender as the outright owner. The key difference from an auction purchase is the transaction process. Buying at auction requires cash, no inspections, and no title guarantees. Buying an REO is a more conventional transaction — the bank lists the property, typically through a real estate agent, and buyers can submit offers, conduct inspections, and obtain financing in most cases. Banks sell REO properties as-is with limited disclosures, but the process is far more accessible to traditional buyers than the courthouse steps auction. In the Austin housing market, REO inventory is tracked as part of the broader 2,483-property distressed pipeline and represents the final stage of the foreclosure cycle.