Austin Luxury Market Update: 80th–90th Percentile Prices Fall Sharply

Published | Posted by Dan Price

Austin’s luxury market is now leading the correction, with top-tier price brackets showing the sharpest year-over-year declines in the city.

The Austin real estate market continues to reshape itself in 2025, and the high end of the price spectrum is experiencing the most visible adjustment. While the broader austin housing market has been softening for more than a year, the latest percentile data confirms that the upper tiers are cooling at a faster pace than the rest of the austin property market. This shift matters for buyers, sellers, and agents because it signals where the pressure is building and how pricing power is changing across different price brackets. The data makes the story clear: Austin’s luxury segment is recalibrating more aggressively than mid-market price points.

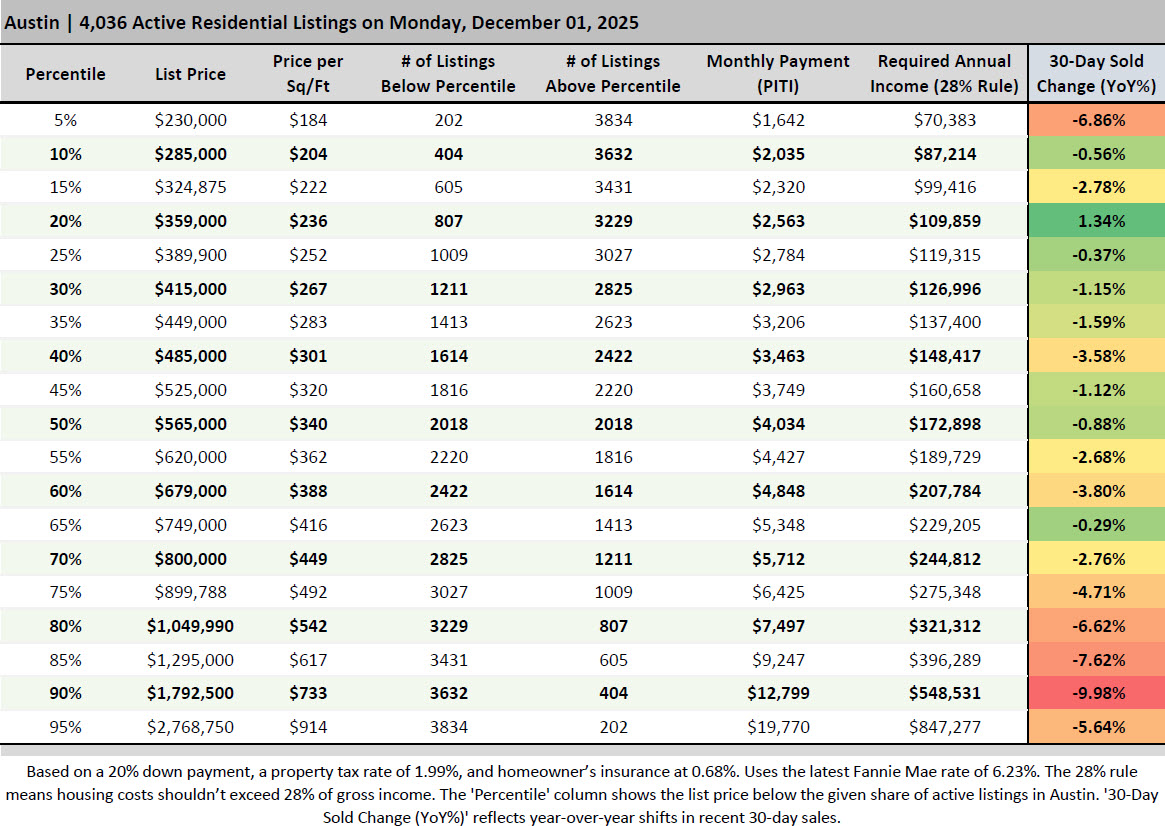

The 80th percentile is now anchored at $1,049,990, representing a year-over-year decline of -6.62 percent. This price point divides the market into two distinct groups, with 3,229 active listings priced below that level and 807 above it. The imbalance illustrates how top-heavy the austin real estate market has become, with a large block of supply stacked in price ranges where the buyer pool is naturally smaller. Homes priced above $1 million have been experiencing longer market times and softer absorption compared to mid-tier listings, and this dataset reinforces that trend.

The correction becomes even more pronounced as the analysis moves deeper into the luxury segment. The 90th percentile begins at $1,792,500, where year-over-year prices have fallen -9.98 percent. This is the steepest decline of all tracked percentiles and signals that affordability constraints are hitting the upper end harder than the middle. There are currently 404 homes priced above this threshold, and this cluster of high-end supply sits in a segment where fewer buyers are writing contracts. These numbers reveal how quickly confidence is fading in the upper echelon of the austin housing market, especially when compared to the resilience seen between the 20th and 60th percentiles.

Market behavior at these higher price points aligns with broader austin real estate trends from late 2024 into 2025, where elevated inventory and cautious demand have been applying downward pressure on austin home prices. Buyers capable of purchasing in the 80th to 90th percentile are more selective, often financially flexible, and typically unwilling to stretch when macroeconomic signals remain mixed. As a result, luxury listings must price correctly and adjust faster to match real-time buyer expectations. Overpricing is punished more severely today than it was during the 2020–2022 boom cycle.

The decline at the 80th and 90th percentiles also fits within the larger austin real estate forecast narrative, which points toward continued normalization after the significant run-up seen during the pandemic surge. Sellers at higher price points are now contending with larger inventory pools and more transparent competition, and buyers have regained control in negotiations, especially on homes above $1.5 million. This environment is producing longer days on market, more price reductions, and a clearer separation between aspirational pricing and realistic market value.

Looking ahead, the top-heavy nature of the austin property market will continue to influence pricing behavior. With 807 homes priced above the 80th percentile and 404 homes above the 90th percentile, luxury inventory is deep enough to keep downward pressure on these ranges unless demand materially strengthens. For buyers, this is one of the most favorable environments for luxury purchasing in years. For sellers, it is an unmistakable signal that pricing strategy, condition, and presentation must be stronger than ever. The market is rewarding accuracy and punishing delay.

Austin’s upper tiers are no longer insulated from correction. They are leading it, and this shift is shaping the trajectory of austin housing trends heading into 2026. The data is clear, and the path forward is straightforward: the luxury segment will continue to influence the broader austin real estate market as it works through elevated supply and recalibrated buyer expectations.

FAQ Section What is driving the decline in Austin’s 80th and 90th percentile home prices?

The decline is primarily driven by a combination of elevated inventory and softer demand at higher price points. Luxury buyers are moving more cautiously due to broader economic uncertainty and higher financing costs. As supply continues to exceed demand in this segment, pricing pressure increases, leading to year-over-year declines across the upper tiers of the austin real estate market.

Is Austin’s luxury market correcting faster than the rest of the city?

Yes. While Austin’s overall market shows moderation, the most pronounced declines are occurring in the 80th to 90th percentile ranges. The -6.62 percent and -9.98 percent year-over-year declines demonstrate that the luxury sector is softening more rapidly than mid-tier segments, which tend to benefit from broader buyer pools and stronger absorption.

How does high-end inventory impact Austin home prices?

A large inventory of homes priced above $1 million increases competition among sellers, especially when buyers have no urgency to act. This results in longer days on market, frequent price reductions, and greater sensitivity to overpricing. Elevated luxury inventory creates downward pressure on austin home prices in those tiers and influences overall market psychology.

What should sellers in the luxury segment expect over the next several months?

Sellers should anticipate a competitive environment where pricing accuracy is essential. With hundreds of comparable listings available and buyer selectiveness increasing, homes must be priced realistically from the start. Condition, staging, and presentation carry more weight, and strategic adjustments are often required to stay aligned with current austin real estate trends.

Is now a good time for buyers to enter Austin’s upper-tier market?

For qualified buyers, the current environment offers more leverage than at any point in recent years. Prices in the 80th and 90th percentiles have declined meaningfully, inventory remains elevated, and competition among buyers is limited. These conditions create opportunities to secure favorable terms while the market continues its normalization phase.