Austin Lease Inventory Breaks Records in July 2025

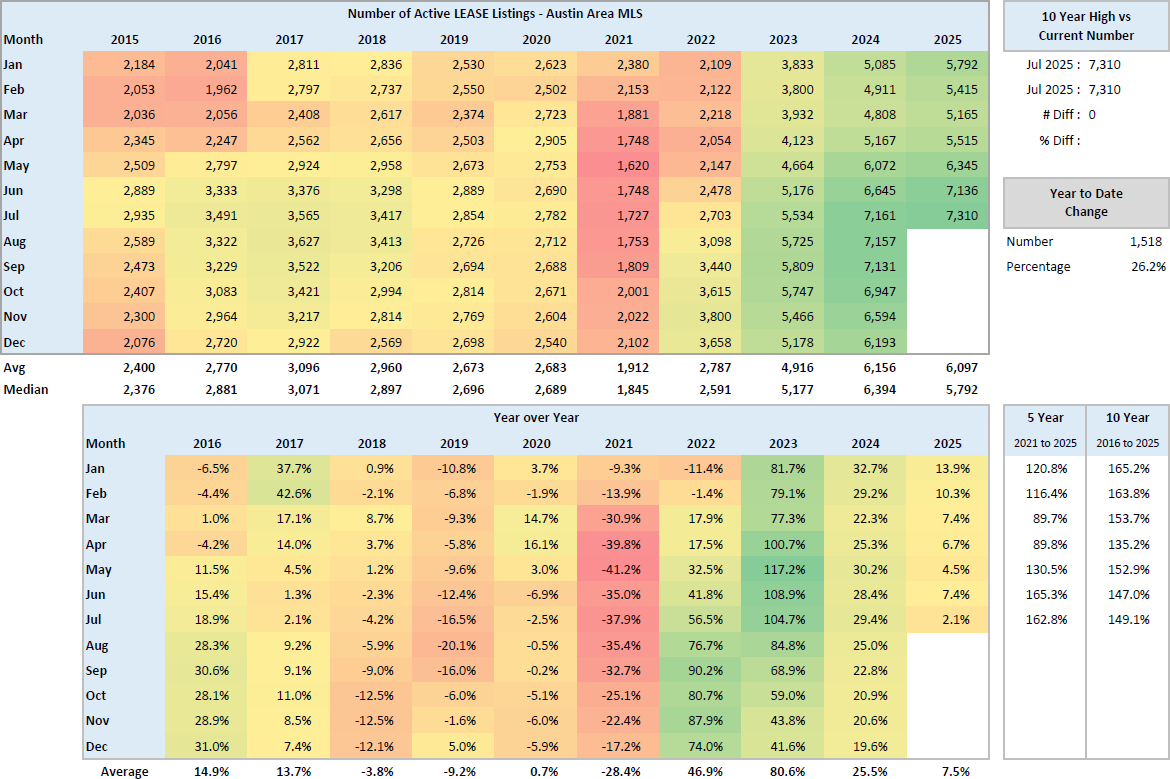

Austin’s rental market just crossed a major threshold. In July 2025, the Austin-Area MLS reported 7,310 active residential lease listings—the highest number ever recorded. This figure surpasses the previous record set in July 2024 and marks a significant shift in the local lease market. The Austin region is now facing an inventory environment that most landlords and renters haven’t seen in over a decade. While market watchers have been anticipating some form of saturation, these latest numbers confirm a true oversupply that is rapidly changing the dynamics between property owners and tenants.

Inventory Growth is Accelerating

To fully grasp the magnitude of the shift, it helps to look at where the market has come from. In July 2021, there were only 1,727 lease listings on the Austin-Area MLS. Four years later, inventory has increased by more than 165 percent. Just two years ago, in July 2023, there were 5,534 active listings. Now, with over 7,300 listings, we’re not just seeing elevated supply—we’re seeing sustained acceleration that defies seasonal expectations. The year-over-year increase from July 2024 to July 2025 may only be 2.1 percent, but the real signal is the consistency in high inventory throughout this entire year. The average number of active listings in 2025 is now more than double the pre-pandemic norm.

Lease Activity is Falling Behind

What makes the inventory spike even more concerning is the fact that demand is not keeping pace. In July 2025, only 2,689 properties were leased across the Austin-Area MLS. That’s a 21.5 percent drop compared to the 3,427 leased in July 2024. In the City of Austin specifically, only 1,440 leases were recorded in July—down 22.7 percent from the same time last year. The result is more listings sitting longer and increasing pressure on landlords to offer concessions, lower rents, or both. The reduced leasing velocity means renters are not just slower to move—they are exercising more discretion and waiting for better deals, further softening demand.

Months of Inventory Signals Oversupply

Months of Inventory is a metric often used in for-sale housing markets, but it applies just as well in leasing. This figure tells us how many months it would take to lease out all available inventory at the current rate of absorption. In July 2025, Austin’s lease market recorded 2.86 months of inventory. A year ago, it was 2.80. In July 2021, it was only 0.84. When the number surpasses 2.5 months, we enter a renter-friendly environment. The upward trajectory over the past three years confirms that the current supply is outpacing the market’s ability to absorb it. This shift in power from landlords to renters will likely continue unless new construction slows dramatically or demand picks up in a sustained way.

Key Factors Driving Inventory Growth

Several structural trends are contributing to this new inventory environment. The first is the continued delivery of new apartment units and single-family rentals across the greater Austin area. Developers in markets like Pflugerville, Leander, Kyle, and South Austin have brought thousands of new units online since 2023. Many of these projects were approved or started during the post-pandemic migration boom and are now hitting the market in a very different economic climate. The second factor is declining migration. While Austin still draws new residents, the volume has cooled substantially compared to 2021 and 2022. Slower in-migration means slower lease-up rates. Third, many homeowners who struggled to sell in today’s high-interest environment have turned to leasing their homes, pushing additional supply into the lease market. Lastly, affordability pressures are slowing renter activity overall. Tenants are staying put longer, doubling up, or moving farther out to reduce cost—adding friction to the leasing process.

Investor and Landlord Implications

Landlords are now competing in a high-inventory market where tenant demand is not matching expectations. Properties that are overpriced or poorly positioned are sitting vacant for longer. Leasing strategy has become mission-critical. Simply listing a property at last year’s rent is no longer sufficient. Landlords should prepare for longer marketing times and plan for incentives such as move-in specials, application waivers, or small rent reductions to remain competitive. For investors, the numbers require more conservative underwriting. Pro forma lease-up assumptions must be adjusted. Cash flow projections should reflect the real possibility of extended vacancies or reduced effective rents. Even seasoned investors who have succeeded in past cycles need to recalibrate their expectations for this new lease environment.

What This Means for Renters

If you’re a renter, this is your market. The surge in available units combined with slower leasing traffic means more negotiating power than renters have had in years. Renters can afford to shop around, ask for discounts, and seek favorable lease terms. Areas with new construction or high recent inventory growth are especially likely to offer concessions. Properties that have been sitting on the market for three weeks or more are likely to be most flexible on pricing or move-in terms. For those who have flexibility in move-in dates or location, the savings opportunities are considerable.

Outlook for the Rest of 2025

The lease market is unlikely to rebalance quickly. There is still significant inventory in the pipeline, and macroeconomic uncertainty continues to suppress renter mobility. While population growth has not stopped, it is no longer surging. New construction deliveries will continue through late 2025 and early 2026. As a result, we expect inventory to remain elevated and concessions to remain common, especially in high-density zones and newer product types. Rents may stabilize at lower effective levels than landlords have grown used to over the past three years.

Final Word

The July 2025 lease inventory milestone is more than a headline—it is a defining moment in the ongoing evolution of the Austin real estate market. Whether you’re an investor evaluating your portfolio, a landlord preparing to list, or a renter exploring your options, understanding this shift is essential. The days of under-supplied rental housing in Austin are behind us for now. With inventory levels at historic highs, pricing and positioning will determine success or failure in the months ahead.

Frequently Asked Questions

What is the current lease inventory in Austin, Texas?

As of July 2025, the Austin-Area MLS reports 7,310 active residential lease listings, the highest total ever recorded. This reflects a 2.1 percent increase year-over-year and more than a 165 percent increase compared to July 2021.

What does 2.86 months of lease inventory mean?

It means that at the current leasing pace, it would take 2.86 months to absorb all the available rental listings. This level is considered oversupplied and typically favors renters, giving them more leverage in lease negotiations.

Why is there such a large increase in rental inventory?

A combination of factors is driving this surge, including the completion of new apartment projects, fewer people relocating to Austin than during the pandemic years, more homeowners leasing out properties that didn’t sell, and overall affordability fatigue among renters.

Are rents going down in Austin?

While official asking rents may not show significant drops yet, many landlords are offering concessions such as free rent or waived fees, effectively lowering the cost to tenants. Renters should negotiate and compare options to take advantage of the softening market.

How should landlords respond to this oversupply?

Landlords should carefully review their pricing strategy, prepare to offer incentives, and expect longer lease-up timelines. With more competition in the market, listing presentation, responsiveness, and pricing flexibility will be critical to attracting quality tenants.