Austin’s housing market is steady on the surface—but the currents underneath are shifting.

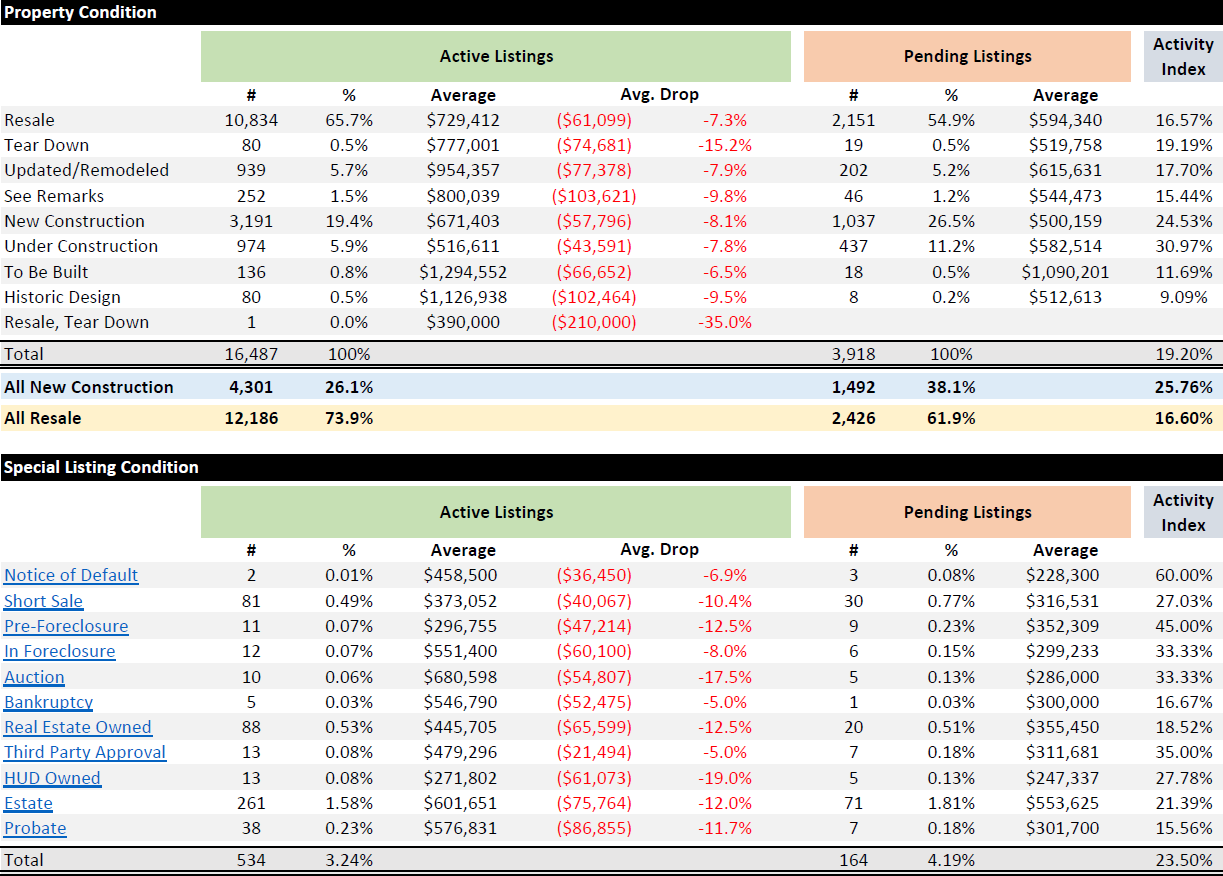

Austin real estate has entered the final quarter with more supply, slower absorption, and price behavior that depends on where you sit in the market ladder. As of October 17, active residential listings across the six-county Austin area stand at 16,487, with 3,918 properties under contract. That puts the Activity Index at 19.2% and Months of Inventory at 5.82—more inventory and a slower pace than a year ago.

The headline is straightforward: Austin housing is still operating below the 2022 price peak, even as day-to-day pricing looks firmer than last winter. Buyers have more to choose from, sellers are competing on value rather than hype, and agents are working in a market where strategy beats speed. Against that local backdrop, the national housing cycle is setting up for a correction phase driven by tighter credit, elevated delinquencies in certain lending segments, and investor pullback from overheated sub-markets. Austin is not immune to national liquidity or sentiment shocks, so the next six to nine months will likely reward disciplined pricing, granular comps, and stronger concessions structures.

Start with supply and flow. Active listings are up roughly mid-teens year over year, while pending contracts are down about four percent compared to last October. That divergence explains why Months of Inventory has drifted from the low-5s to the high-5s. A 5.82 MOI is not a collapse; it’s a market that is both negotiable and selective. The absorption gap also shows up in price-change behavior: nearly six in ten active listings across the MLS have taken at least one price reduction this cycle, a clear sign that list prices are still reaching above what buyers are willing to pay on first pass. New construction remains a major swing factor—roughly a quarter of all active listings and nearly two-fifths of pendings—because builders can use buydowns and incentives to produce “payment wins” even when nominal prices appear steady.

Price level versus price path matters. The Austin market remains below its May 2022 peak values; that gap is the important macro anchor for affordability and for investor underwriting. Month to date, average and median sold prices are running warmer than they will likely finish because higher-priced transactions tend to close earlier in the month and lower-priced deals load in the back half. As the rest of October posts, mix will likely pull the preliminary figures down. The takeaway for sellers is to ignore early-month noise and focus on the last-90-day comp set; for buyers, don’t chase “hot” mid-month averages when your sub-market tells a cooler story.

Now layer in the national setup. Several forces are coalescing into a broad correction: credit standards have tightened at the margin, early-stage delinquencies are off the floor, and investor demand is thinner in Sun Belt metros that overbuilt or leaned too hard on short-term rental returns. When capital gets more cautious, the first order effect is slower absorption; the second is wider spreads between pristine and average homes; the third is policy and program “work-arounds” that help some buyers but don’t lift the entire market. In practice, that shows up as growing variability across neighborhoods and price bands. Austin has already been living with that two-track reality—updated, well-located listings still find the market; dated or mis-positioned inventory finances the buyer through price cuts, concessions, or buydowns.

Inventory mix is the tells-all chart. With 26% of actives in new construction and that segment accounting for 38% of pendings, builders are acting as price-to-payment routers. They’re moving units with rate buydowns and closing credits that individual sellers struggle to match. That doesn’t mean resale can’t compete; it means resale needs to win on presentation, pricing precision, and value framing. If you’re listing a home that’s cosmetically behind your comp set, your real competition isn’t the resale down the street—it’s the builder down the highway offering a two-one buydown and appliances at closing.

Geographic dispersion adds another layer. Sub-markets with heavy 2021–2022 build pipelines or investor clusters will feel more national cyclicality in Q4 and into early 2026. That’s where days on market expand first and where sold-to-list ratios erode fastest. Conversely, close-in neighborhoods with scarce supply and strong school footprints tend to hold better, even as buyers negotiate for repairs and credits. In other words, the national correction narrative doesn’t “hit Austin” all at once; it filters through the weak points in the system—overbuilt edges, investor-dense pockets, and product that hasn’t kept up with today’s buyer expectations.

What should each side do now? Sellers should price to the market that exists, not the one they hoped for in spring. The goal is to be the best value in your immediate comp set on day one, then defend that position with small, timely adjustments rather than a large capitulation after 30 days. Recognize that more than half of your competition has already dropped at least once; buyers are trained to expect movement, so factor a concession path into your launch plan. Buyers should treat the current Austin housing market as an opportunity to buy quality at a discount to peak, but they need to stay disciplined: underwrite payment with today’s rate, ask for credits to neutralize inspection findings, and be patient with homes that are clearly out of step with their sub-market. Investors should pick their spots, prioritize cash flow over appreciation, and avoid capex traps masked by attractive entry prices.

For agents and analysts, the daily playbook is simple. Lead with the numbers—actives up, pendings down, Activity Index sub-20, MOI near 5.8—and then localize the story to the block level. Replace generic “price is up/down” language with segment-specific signals: Have median days on market extended in your ZIP? Are builder incentives compressing effective monthly payments more than resale price cuts? Are repairs and seller credits out-performing list-price reductions in your negotiation history? Your competitive advantage this winter is translating those signals into clean client choices.

If the national cycle does progress toward a correction, the path in Austin likely looks like this: liquidity thins first, list-to-sold negotiation widens next, and then price indices reflect the change with a lag. Because we’re already below the 2022 peak, the local story is less about a sudden drop and more about whether we grind sideways in nominal terms while affordability quietly improves through incentives and mix. That’s the base case. The tail risk—one we’ll monitor in real time—is a sharper national credit event that temporarily freezes transaction volume. If that happens, Austin’s best-in-class inventory will still clear, but the spread to average homes will widen further until pricing and presentation adjust.

In short, Austin housing is stable but sensitive. Supply is higher, absorption is slower, and pricing power now belongs to the best-positioned homes and the most prepared buyers. The city is still below its peak, which is a feature, not a bug, for long-term affordability. With rigorous comps, honest pricing, and smart use of concessions, both sides can win into year-end.

FAQ

Is the Austin real estate market cooling right now?

Yes, in the sense that more listings are competing for fewer buyers than last year. Active inventory is higher, pending contracts are slightly lower, and Months of Inventory sits near the upper-5s, which signals a negotiating market rather than a frenzy. The best homes still trade quickly, but average listings need sharper pricing and concessions to move.

Are Austin home prices dropping?

Prices remain below the 2022 peak, and day-to-day movement depends on segment and mix. Early in each month, higher-priced closings can make averages look warm; as lower-priced sales post later, month-end prices often settle. Focus on the last 90 days of comps in your sub-market to understand true direction.

How would a national housing correction affect Austin?

The first impacts would likely be slower absorption, wider gaps between top-tier and average homes, and more aggressive concessions from builders. Investor-heavy or overbuilt edges of the metro would feel pressure first, while close-in, supply-constrained neighborhoods would hold better. The degree of impact depends on credit conditions and employment stability.

Is now a good time to buy in Austin?

If you’re payment-driven and buying for the next five to seven years, the combination of below-peak prices and negotiable terms can work in your favor. Use seller credits and buydowns to optimize monthly payments, and avoid properties with deferred maintenance that will erase your savings after closing.

What’s the Austin real estate forecast for the next six months?

Expect a selective, data-driven market: inventory elevated, absorption steady-to-soft, and price outcomes tied to condition and location. If national credit tightens further, concessions will expand and days on market will lengthen; if rates ease, builders and well-priced resale listings will capture demand first.