Austin Housing Market Update: Absorption Falls to 10-Year Low in November 2025

Published | Posted by Dan Price

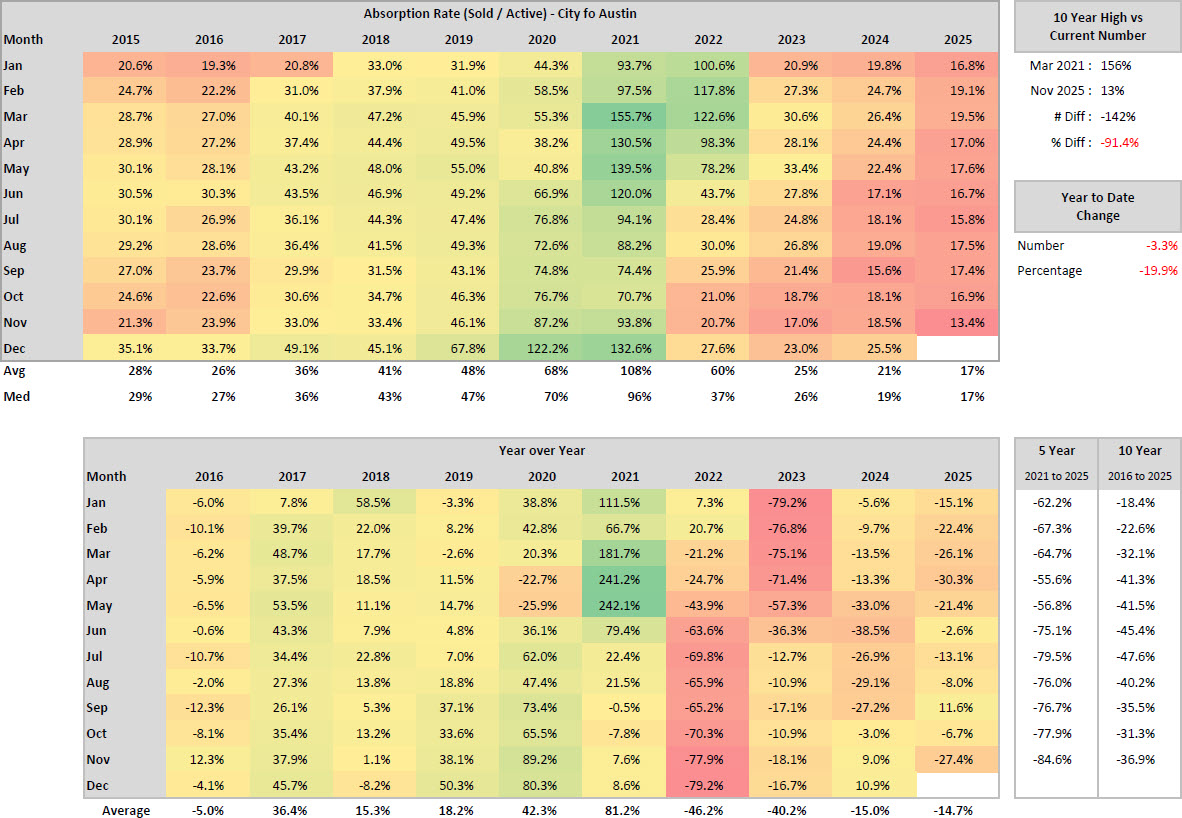

In Austin’s real estate market, the absorption rate has fallen to a point that clearly confirms buyer dominance as we approach 2026. November 2025 registered an absorption rate of just 13.4 percent, which is the lowest November recorded in at least ten years. For comparison, November 2021 absorbed 87.2 percent of available listings and the historic peak in March 2021 reached an absorption rate of 155.7 percent. Compared to that peak demand moment, current absorption is down by more than ninety one percent. This data demonstrates not only a correction phase but a structural shift. The level of buyer selectivity and the degree of pricing competition now required to secure a sale are unlike any point in the last decade.

Throughout 2025 the market averaged an absorption rate of only 17 percent. By perspective, 2021 averaged 108 percent and 2022 averaged 60 percent. Even during weaker cycles, Austin historically maintained absorption between 43 and 61 percent from April through June. This year those months only saw an average of 17.7 percent. The sustained decline suggests that even seasonal strength cannot offset the broad imbalance between supply and demand. New construction continues to price aggressively and often below resale levels, especially once incentives are applied. As a result, resale inventory is forced to identify value positioning early or face extended market time.

Year over year performance reinforces the market’s continued downward pressure. November 2025 absorption is down 27.4 percent compared to November 2024. The largest single year contraction occurred in 2023 when the November absorption rate fell by over 77 percent. While 2024 briefly appeared to slow the decline, 2025 confirms that stabilization has not taken hold. Over the past five years absorption is down by more than 62 percent and compared to the ten year range absorption remains down by more than 41 percent. These declines highlight that current market behavior is not a temporary slowdown but a realignment of demand dynamics following the inflated levels experienced during early 2021.

The current ratio of homes selling compared to available inventory reflects an environment where only one out of every seven active listings goes under contract during the month. In these conditions buyers carry greater negotiation leverage. Sellers waiting for the market to improve before adjusting pricing often trail the competition rather than leading it. Correct strategic positioning must happen early in the listing cycle rather than relying on reactive price reductions. Listings that identify clear value alignment at launch set the new comparable benchmarks. Those that do not tend to chase the market down.

This low absorption environment also influences future inventory projections. If absorption does not rise above 25 percent and ideally approach 30 percent for multiple consecutive months starting in the first quarter of 2026, active inventory could expand beyond the twenty thousand unit threshold by mid to late 2026. Should that occur, builders would likely carry increased pricing authority. Their ability to structure incentives and deliver inventory quickly creates competitive pressure that resale sellers cannot match without proactive pricing strategy. This reinforces the expectation for ongoing price pressure unless demand meaningfully accelerates soon.

Agents and sellers must adjust to this operating environment. Rather than waiting for signals of stabilization, decisions should be based on the current absorption rate which indicates that the correction phase is still active. Sellers should focus on setting competitive list prices supported by strong presentation. Buyers continue to benefit from negotiation leverage and increased selection. Investors may find opportunities at properties that have experienced prolonged market times or multiple price reductions. For those purchases, the ability to negotiate terms can support long term performance expectations.

The absorption data shows that while pricing declines have slowed compared to the initial correction period, market performance does not yet show signs of measurable recovery. Until demand accelerates beyond current thresholds, pricing normalization remains unlikely. The next six months will be critical in determining whether Austin begins to stabilize or enters a second phase of correction. As of now, absorption trends support a cautious and strategic approach rather than one driven by optimism. The most effective path forward is early alignment with market reality, not gradual adaptation.

In summary, Austin’s November 2025 absorption rate reflects ongoing buyer control and sustained pricing pressure. With current absorption at its lowest point in a decade and only 13.4 percent of inventory selling each month, sellers must prioritize strategic positioning from day one. Until absorption levels consistently break above the stabilization range, the market will continue to operate in correction mode. This data sets the foundation for the 2026 market narrative and confirms that demand has not yet recovered enough to shift conditions toward price support.

Frequently Asked Questions

What does a 13.4 percent absorption rate mean for the Austin housing market

A 13.4 percent absorption rate means that only a small fraction of available listings are selling each month. This indicates high inventory levels relative to demand and confirms that buyers have strong leverage in negotiations. Homes that are not priced correctly at the start often spend extended time on market.

How does this absorption level affect home prices

Lower absorption typically leads to increased pricing pressure as more sellers compete for fewer buyers. When one out of seven homes sells each month, pricing must align with buyer expectations immediately. Properties that overreach or rely on gradual adjustments often close below their potential market value.

Is this a good time to buy in Austin

Current market conditions favor buyers and data driven investors. Absorption at this level allows buyers to negotiate more favorable terms and select from a wider range of inventory. Homes with extended days on market or multiple reductions may present strong opportunity windows.

When could the Austin market begin to stabilize

Stabilization typically requires sustained absorption above 25 percent and ideally closer to 30 percent. With current averages near 17 percent year to date, the market is not yet on a recovery trajectory. The first quarter of 2026 will be critical for determining whether demand improves enough to support stabilization.

How should sellers approach pricing in this market

Sellers should lead with competitive pricing rather than waiting for the market to validate their position. Data indicates that early alignment with buyer expectations creates stronger negotiation outcomes. Homes that adjust late often track the precedent set by more aggressively priced listings.