Austin Housing Market Update: Cumulative Trends Show Supply Outpacing Demand

Published | Posted by Dan Price

The Austin housing market continues to move through one of the most statistically revealing years we’ve seen since the post-pandemic normalization phase began, and the latest cumulative data through November shows demand holding steady but not accelerating, while listing volume continues to outperform historical norms.

Austin’s real estate activity, when viewed through cumulative metrics instead of month-to-month volatility, gives a clearer read on the underlying direction of the market. These long-horizon indicators show that buyers are still engaging, but at a pace below the region’s long-term trend. At the same time, new listings are being added at a rate that is materially higher than what Austin typically produces. This imbalance between new supply and slower cumulative pending activity remains one of the defining features of the 2025 Austin real estate market.

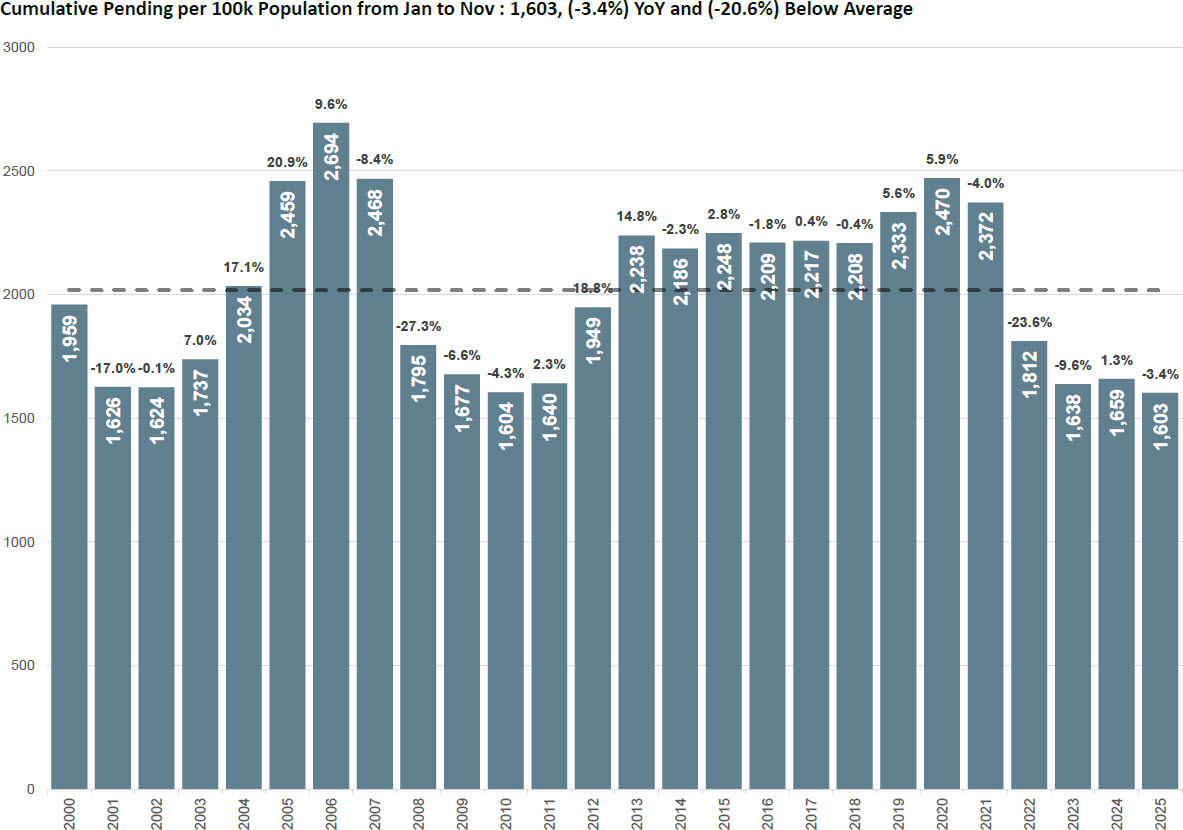

The most important demand metric in this dataset is cumulative pending contracts per 100,000 population. Through November, Austin recorded 1,603 cumulative pending per 100,000 residents. That figure represents a 3.4 percent decrease from last year and sits more than 20 percent below Austin’s long-term average. This is a significant gap, and it clearly shows that buyer engagement is steady but not strong enough to counteract the higher rate of incoming listings. While pendings are not collapsing, they are operating in a muted band, which is consistent with a market still normalizing rather than expanding.

Another way to view buyer activity is through raw cumulative pending totals. So far this year, Austin has posted 41,025 cumulative pending contracts from January through November. That number is down just 1 percent year over year, which underscores a key point about the Austin housing market. Even though per-capita demand remains well below the long-term trend, total demand has not materially deteriorated. In fact, cumulative pendings are 7.2 percent above their long-term average, which indicates that absolute transaction volume remains healthier than many observers might expect. The challenge is not that demand is weak; it is that it is not growing fast enough to keep up with the amount of new supply entering the system.

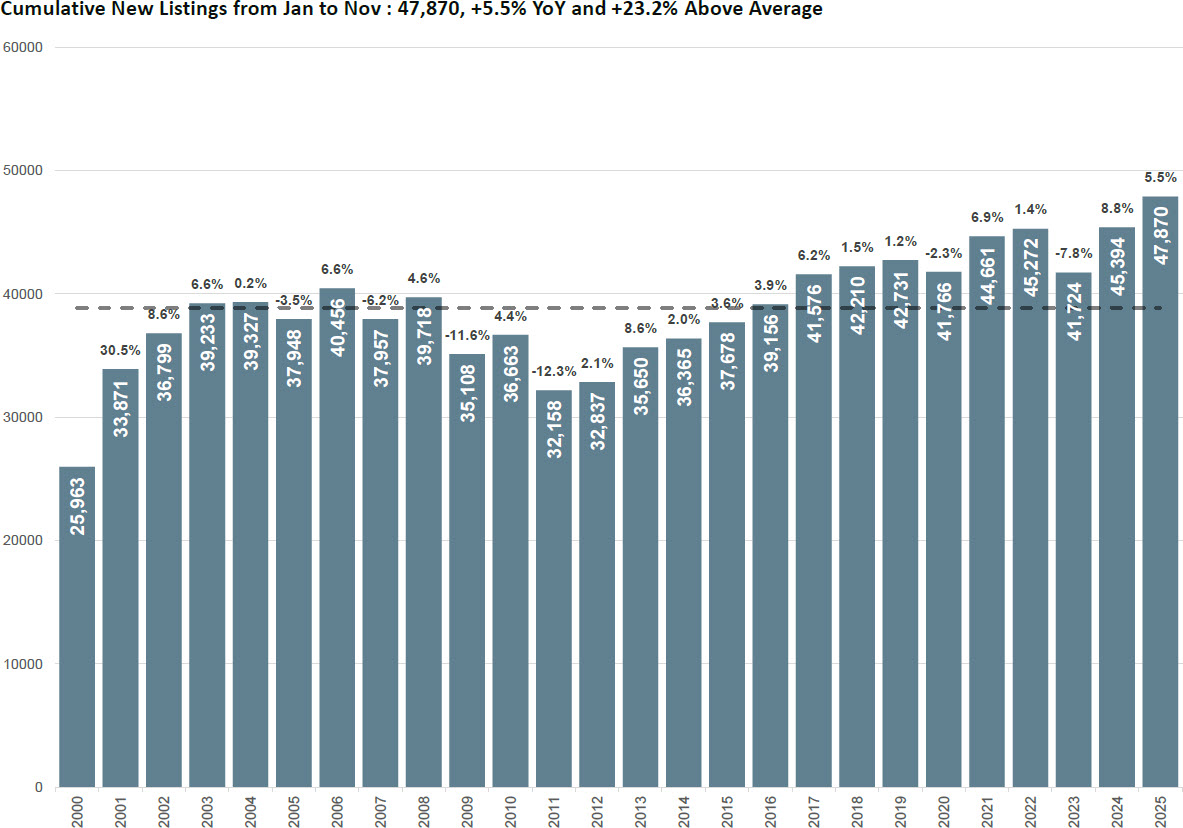

On the supply side, the cumulative new listings picture is one of the most important storylines of 2025. Austin has recorded 47,870 new listings from January through November, which is a 5.5 percent increase year over year and more than 23 percent above the long-term average. This is a substantial difference and represents a clear shift in seller behavior. Homeowners who previously stayed on the sidelines are now more willing to list. Builders continue to contribute heavily to the overall supply picture, and resale listings have risen meaningfully compared to the post-2022 lull. When cumulative new listings run more than twenty percent above trend, the market naturally absorbs that pressure through softer prices, longer market times, and a more selective pool of buyers.

A useful complementary metric is cumulative new listings per 100,000 population. Through November, Austin has produced 1,871 new listings per 100,000 residents. This represents a 3 percent year-over-year increase but remains more than 11 percent below the long-term average on a per-capita basis. This gap highlights the tension between absolute supply and population-adjusted supply. Raw listing activity is far above normal, but per-capita listing activity is still below historical trends because population growth in Austin has been so strong over the past decade. The interplay between these two viewpoints—absolute versus per-capita—helps explain why today’s Austin housing market feels simultaneously well-supplied and yet not structurally oversupplied at the population level.

When you combine these metrics, the story becomes clearer. Absolute demand is holding, but per-capita demand remains below trend. At the same time, absolute new listing activity is elevated far above historical norms, while per-capita new listings remain lower because the metro continues to grow. The imbalance is not severe enough to signal distress, but it is significant enough to keep Austin in a neutral-to-softening housing environment. Buyers are selective. Sellers must price realistically. And the market is moving at a measured, steady pace rather than showing signs of acceleration.

The cumulative perspective also removes much of the noise associated with interest rate swings and seasonal shifts. Even though mortgage rates have fluctuated this year, cumulative pending activity has remained remarkably stable, drifting only slightly lower year over year. This stability reinforces the idea that Austin has settled into a post-pandemic baseline. Buyers remain active, but they are no longer rushing, and they are no longer willing to chase prices beyond affordability thresholds. Cumulative pending data confirms that the pace of accepted contracts reflects a market that is functioning normally but not expanding.

Inventory pressure will continue as long as new listings outpace pending demand. When cumulative new listings run more than 23 percent above average while cumulative pending per 100,000 population runs more than 20 percent below average, the directional bias of the market is clear. The Austin housing market is not in a growth cycle. It is in a balancing cycle defined by normalization, slower price appreciation, and increased negotiating leverage for buyers. Sellers who price ahead of the market will face longer days on market and potential price reductions. Sellers who price to today’s environment will continue to attract the most serious buyers.

Looking ahead, the cumulative data suggests that Austin’s real estate market is unlikely to overheat in the short term. Instead, it is positioned to continue its steady normalization trajectory. The gap between per-capita pendings and per-capita new listings means inventory is likely to remain elevated, even if rates ease slightly. The Austin property market will continue to reward realistic pricing strategies and accurate expectation-setting for both buyers and sellers. In short, Austin’s housing trends reflect a region that is stabilizing after several years of extreme volatility, and the data shows a market that is moving toward long-term equilibrium rather than breaking out into a new cycle of rapid expansion.

FAQ

What does “cumulative pending” tell us about the Austin housing market?

Cumulative pending contracts measure the total number of accepted offers over a defined period, providing a clearer view of overall buyer engagement than month-to-month volatility. Austin’s cumulative pending pace shows that demand is steady but not accelerating, which aligns with a neutral market environment. This helps frame how buyers are behaving across the full year rather than in isolated months.

Why is per-capita data important when evaluating Austin housing trends?

Per-capita metrics adjust activity relative to population size, which is critical in a fast-growing metro like Austin. Raw listing and pending counts may appear strong, but per-capita figures often reveal whether the market is keeping pace with population growth. Austin’s per-capita pendings remain below trend, showing demand is stable but not expanding in proportion to metro growth.

How do elevated new listings affect Austin home prices?

When cumulative new listings significantly outpace pending demand, inventory tends to rise, creating downward pressure on prices or at least reducing the rate of appreciation. Austin’s new listings are more than twenty percent above long-term norms, which increases buyer leverage and contributes to softer pricing dynamics across many neighborhoods.

Is buyer demand weakening in Austin?

Buyer demand is not collapsing; cumulative pendings are only down 1 percent year over year and are actually above the long-term average in absolute terms. The issue is that demand is not growing fast enough to offset higher listing activity. This results in a balanced-to-soft market rather than a weakening one.

What does this mean for the Austin real estate forecast going into next year?

The cumulative trends point toward continued normalization rather than a new growth cycle. Elevated listing activity, steady but moderate demand, and softer price momentum suggest the Austin real estate market will maintain a neutral posture. Conditions are unlikely to tighten until buyer activity increases or new listing volume declines.