Austin’s Shadow Inventory: Foreclosures and Short Sales Are Quietly Rising

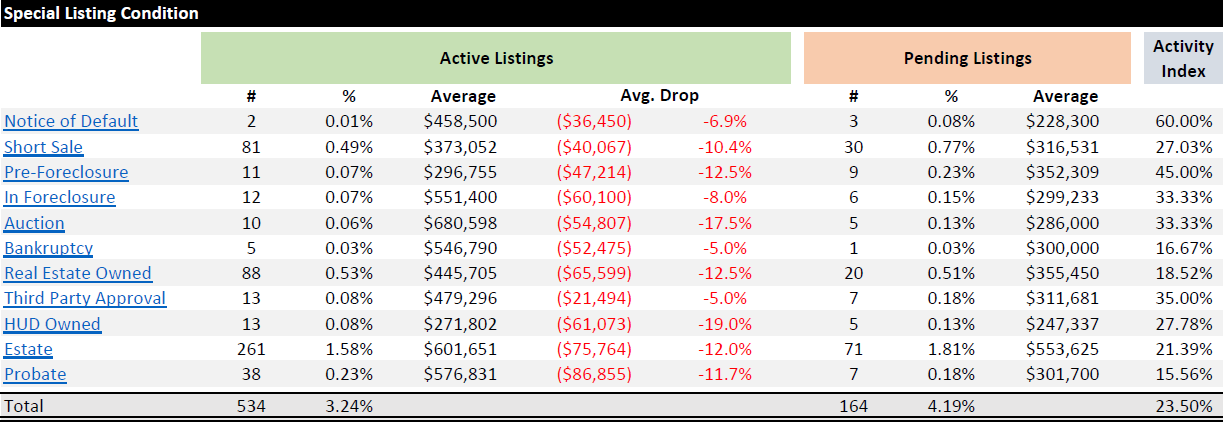

Austin’s real estate market continues to look stable on the surface, but beneath that stability lies a quiet rise in distressed listings—properties tagged as foreclosure, pre-foreclosure, short sale, or real-estate-owned (REO). As of October 17 2025, there are 81 active short-sale listings, 11 pre-foreclosures, 12 in foreclosure, and 88 REO (bank-owned) homes scattered across the six-county Austin area. Add a handful of auction, bankruptcy, HUD-owned, probate, and estate sales, and you get more than 250 distressed or court-controlled properties currently on the market. That number is still modest compared with the total 16,000-plus active listings across the MLS, but it’s the most visible accumulation of distressed supply since 2013. It’s a reminder that while Austin avoided the large-scale defaults that defined the 2008 crisis, financial stress is gradually re-emerging—especially in the outer counties where rapid 2021–2022 building left thin equity buffers.

Short Sales: The First Warning Sign

Short sales make up the largest portion of Austin’s distressed inventory. The 81 active short-sale listings show an average price of roughly $462,000 and an average price cut near 7 percent. Most are concentrated in Austin, Kyle, Hutto, Georgetown, and Elgin, markets that saw aggressive price growth during the 2021 run-up. Short sales appear when homeowners owe more than they can sell for, which means price recovery hasn’t caught up with their loan balances. They are the early warning indicator that equity margins are compressing again. Historically, short-sale listings surge one to two quarters before broader foreclosure filings, as sellers try to exit before the lender steps in. The current volume is small in absolute terms, but its reappearance—after nearly a decade of near-zero activity—marks a shift from “no distress” to “selective distress.”

Foreclosures: Still Contained, but Trending Up

Eleven listings are marked as pre-foreclosure, mostly clustered in Austin, Elgin, Kyle, and Manor, with average price drops between -6 percent and -13 percent. Another twelve properties are formally listed as “In Foreclosure.” The group includes addresses in Austin, Georgetown, Kyle, Lago Vista, and Manor, averaging -6.6 percent price reductions and a median list price near $675,000. The mix ranges from a few under-$300 k starter homes to higher-end West Austin and Lake Travis properties—proof that leverage isn’t confined to the entry-level segment. The bank-owned (REO) category adds 88 homes, many priced between $300,000 and $500,000, with an average discount of -9.7 percent. While REO volumes remain small relative to the total MLS count, they’re now double what Austin carried at the same point in 2024. These are properties that have completed the foreclosure process and reverted to lender ownership—a lagging indicator of prior distress rather than new weakness.

Market Context

Even with these increases, distressed listings represent roughly 1.5 percent of all active inventory. That’s nowhere near systemic danger levels. But the direction matters: defaults are ticking higher just as national data shows delinquencies rising across FHA and non-bank servicers. Austin’s foreclosure-rate movement usually trails the national trend by about six months, so the local numbers could edge higher into early 2026 before stabilizing. The distribution of distress also aligns with affordability stress. Peripheral markets—Jarrell, Kyle, Hutto, Bastrop—carry higher concentrations of FHA and USDA loans made at 2021–2022 prices. Those loans now face payment resets and reduced equity cushions. Core Austin neighborhoods, with stronger incomes and lower loan-to-value ratios, remain comparatively insulated.

What It Means for Buyers, Sellers, and Agents

For buyers, this is an opening to find discounted inventory, but distressed doesn’t always mean deal: banks and loss-mitigation departments move slowly, and inspection contingencies can be limited. Cash or flexible-financing buyers have the upper hand in REO and auction scenarios. For sellers, the presence of more short sales means price discipline is critical. Competing against lender-motivated listings requires sharper pricing and cleaner presentation. Appraisals in areas with multiple distressed comps can lag list prices, extending closing timelines. For agents, tracking this segment is becoming essential again. Monitoring “special listing condition” tags gives early visibility into where stress is building and which sub-markets might soften next.

Outlook

The takeaway isn’t alarm—it’s awareness. Austin’s distressed-listing count is rising from a historically low base, reflecting the normalization of credit risk after years of artificially suppressed defaults. If national delinquency trends continue to climb through 2026, expect a slow but steady increase in pre-foreclosure and REO supply. That could help relieve the region’s affordability crunch, even as it pressures headline pricing in the lower- to mid-tiers. For now, Austin remains well short of any “foreclosure wave,” but the first ripples have appeared.

FAQ

How many distressed properties are on the market in the Austin area right now?

As of October 17 2025, there are 81 short-sale listings, 11 pre-foreclosures, 12 properties in foreclosure, and 88 REO (bank-owned) homes across the six-county Austin area—about 1.5 percent of total inventory.

Are foreclosure levels close to 2008 levels?

No. During the 2008–2011 cycle, Austin-area MLS foreclosure and short-sale counts exceeded 1,000 listings. Today’s combined total is under 200. The rise is meaningful trend-wise but nowhere near crisis scale.

Which Austin sub-markets show the most distressed activity?

Kyle, Hutto, Elgin, Bastrop, and Jarrell have the highest concentrations, while central Austin and Williamson County suburbs like Cedar Park and Leander show only isolated cases.

Do rising foreclosures mean Austin home prices will drop again?

Not directly. With distressed listings under 2 percent of supply, they influence local pricing mainly through comps and sentiment. A broader decline would require a jump in delinquencies and forced sales across mainstream segments.

What’s the outlook for 2026?

Expect a gradual increase in pre-foreclosure and REO activity as pandemic-era forbearance and low-equity loans age out. This could expand lower-priced inventory, improving affordability but keeping price appreciation muted through next year.