Adjustable Rate Mortgage: Pros, Cons, and Current Rates

Published | Posted by Dan Price

Adjustable Rate Mortgage: Pros, Cons, and Current Rates

Adjustable rate mortgages, or ARMs, have been a popular financing option for many homebuyers due to their lower initial interest rates compared to fixed-rate mortgages. With an ARM, the interest rate and monthly payment can change periodically over the life of the loan, which may result in savings in the short term. However, ARMs also come with risks and uncertainties that borrowers should be aware of before deciding on this type of loan.

One of the advantages of an adjustable-rate mortgage is the lower initial interest rate. For borrowers who plan to stay in their home for a short period of time, an ARM may offer lower monthly payments compared to a fixed-rate mortgage, resulting in potential savings. ARMs also offer flexibility in loan terms and payments, which may be beneficial for some borrowers.

However, there are also significant disadvantages to ARMs. Interest rates and payments can fluctuate over time, which means that borrowers may experience higher payments in the future. This can be particularly risky for borrowers who plan to stay in their home for a longer period of time. Additionally, negative amortization can occur when the monthly payment is not enough to cover the interest owed, leading to an increase in the loan balance over time.

Common types of ARMs include 3-year, 5-year, 7-year, and 10-year ARM mortgages. The interest-only ARM mortgage is another type of ARM, where borrowers are only required to pay the interest on the loan for a set period of time. This can result in lower monthly payments in the short term, but can also lead to higher payments in the future.

So, when is an ARM a good idea? For borrowers who plan to own their home for a short period of time or expect their income to increase in the future, an ARM may be a viable option. Additionally, when interest rates are low, borrowers may be able to take advantage of the lower initial interest rate offered by an ARM.

However, when interest rates are high or borrowers plan to own their home for a longer period of time, an ARM may not be a good idea. Risk-averse borrowers may prefer the certainty of a fixed monthly payment, rather than the uncertainty of an ARM.

When choosing between an ARM and a fixed-rate mortgage, it's important to consider the pros and cons of each option. While ARMs offer lower initial interest rates and flexible loan terms, fixed-rate mortgages offer the stability of a consistent monthly payment over the life of the loan.

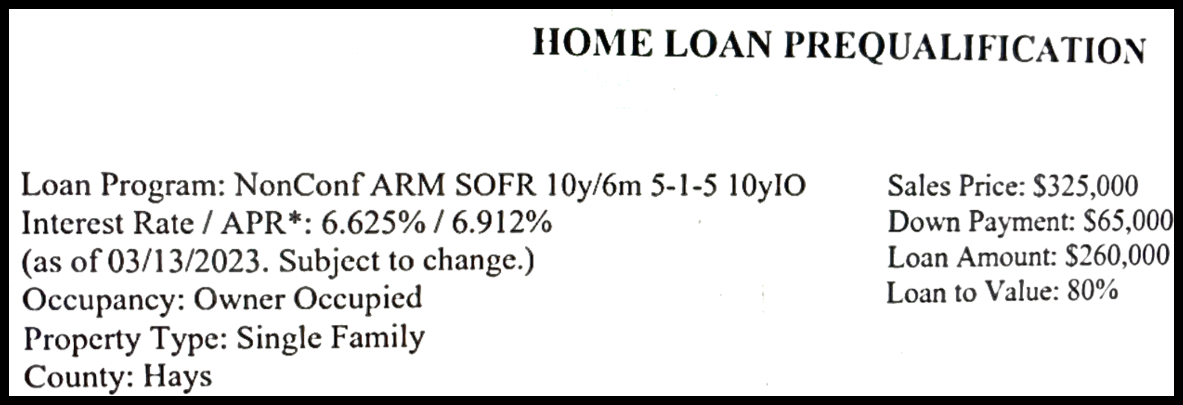

Here is an illustration of a pre-qualification for an adjustable-rate mortgage. The specific type of mortgage is a non-conforming adjustable-rate mortgage that is based on the SOFR benchmark, with a fixed interest rate for the initial 10-year period and a reset period of 6 months. The mortgage has a cap on the maximum interest rate changes, which is 5% after the initial 10 years, and a maximum lifetime interest rate change of 5%. Additionally, there is an initial interest-only payment period of 10 years. Below, you will find a detailed explanation of what these terms mean.

NonConf: This refers to a "non-conforming" loan, which means that it does not conform to the standard underwriting guidelines of government-sponsored entities like Fannie Mae and Freddie Mac. Non-conforming loans often have higher interest rates and stricter qualifying requirements.

ARM: This stands for "adjustable-rate mortgage." An ARM is a type of mortgage loan where the interest rate can change over time based on market conditions.

SOFR: This stands for the "Secured Overnight Financing Rate." SOFR is a benchmark interest rate that is used as an alternative to LIBOR (the London Interbank Offered Rate), which is being phased out. SOFR is based on actual transactions in the overnight repo market.

10y/6m: This refers to the interest rate reset period for the ARM. In this case, the interest rate would be fixed for 10 years, and then reset every 6 months after that.

5-1-5: This refers to the caps on the interest rate changes. The first "5" means that the interest rate can only change by a maximum of 5% after the initial fixed period (in this case, the first 10 years). The "1" means that the interest rate can only change by a maximum of 1% for each subsequent adjustment period. The final "5" means that the interest rate can only change by a maximum of 5% over the life of the loan.

10yIO: This refers to the initial interest-only period for the ARM. During this time, the borrower would only be required to make interest payments on the loan, and would not be required to pay down any principal.

If you currently have an ARM and are considering refinancing, it's important to weigh the advantages and disadvantages of refinancing. ARM refinance rates may be lower than your current interest rate, but it's important to consider any fees associated with refinancing and how long you plan to stay in your home.

As of today, Friday, March 17, 2023 at 7:14 PM, the current ARM rates are fluctuating. Specifically, 5/1 ARM rates are at 5.77%, 7/1 ARM rates are at 6.18%, and 10/1 ARM rates are at 6.47%. It's important to note that these rates can change frequently, and for up-to-date rates, it's best to contact us and speak with a local and trusted mortgage professional. Our team works with a network of reputable lenders in the Austin area and can provide you with the most current and competitive rates available.

Product

Interest Rate

APR

5/1 ARM

5.77%

7.16%

7/1 ARM

6.18%

7.05%

10/1 ARM

6.47%

7.01%

Rates as of Friday, March 17, 2023 at 7:14 PM

Adjustable-rate mortgages can be a viable option for some homebuyers, but come with significant risks and uncertainties. Before deciding on an ARM, borrowers should carefully consider their financial situation, long-term homeownership plans, and the current state of the housing and mortgage markets. Consulting with a trusted mortgage professional can also help borrowers make an informed decision.

If you are considering an adjustable rate mortgage and would like to be connected with a local and trusted mortgage professional, our team is here to help. We work with a network of respected and reputable mortgage professionals in the Austin area and would be happy to provide referrals based on your individual needs and circumstances. Don't hesitate to reach out to us for assistance in finding the right financing option for your home purchase.

Related Articles

Keep reading other bits of knowledge from our team.

Request Info

Have a question about this article or want to learn more?